Decision-making structures in consulting, investment and asset allocation in the family office sector are viewed with great interest by product providers and investors. In the market segment Multi Family Offices, too, know-how is being continuously expanded in the area of liquid and illiquid products. Markus Hill spoke on behalf of FONDSBOUTIQUEN.DE with Dr. Christoph Pitschke, Head of Real Estate and Investments, Deutsche Oppenheim Family Office AG, about the in-house advisory process, strategic asset allocation (SAA), asset reporting and topics such as real estate investments. In addition, topics such as the selection of products such as liquid funds, private equity and venture capital, club deals and the current development and increasing importance of ESG, SRI and impact investing were also addressed.

Hill: How does Deutsche Oppenheim take illiquid asset classes into account when advising families?

Pitschke: As a multi-family office, we advise our clients with a cross-generational view of their entire assets. For us, the central instrument of asset management is the so-called Strategic Asset Allocation (SAA). This divides the investment universe into different asset classes with their respective desired investment volumes and risk/return profiles. By simulating expected values for individual asset classes in terms of risk and return, asset allocations are determined for the entire portfolio together with the client families. Based on the SAA, a dedicated strategy can be defined for each asset class, which we implement together with our clients. The basis for cross-generational asset management is efficient asset reporting. This is our core service with which we primarily reduce complexity, which is more or less pronounced in the case of large assets. One of our strengths lies in the fact that our real estate and investment reporting also allows us to precisely depict illiquid asset classes in our total assets. Experience shows that ongoing reporting provides the right framework for strategy implementation and efficient real estate management. The individual consulting segments are available from us in their entirety, but also individually, i.e. as modules.

Source: Deutsche Oppenheim Family Office AG

In regular discussions on strategy and asset reporting, we have repeatedly received requests from our clients in recent years to invest in tangible assets and especially in real estate. With a portfolio share of around 20%, high net worth individuals are much more heavily invested in real estate than most institutional investors and they continue to buy rather than sell.

Hill: How do you select real estate objects in-house?

Pitschke: Crucial for successful real estate transactions is an understanding of the client’s initial situation and target system. As is also usual in institutional business, we first try to define the defined strategy together with the families, quasi as “investment guidelines”, and also write it down. Here, our aim is to determine exactly where the property should be located, what type of property is being sought and what investment size will be involved. On this basis, a targeted search for the right property is possible. This enables us to select incoming offers in a structured way and also to contact potential sellers. When acquiring individual, directly held properties, however, it must be questioned to what extent efficient diversification is possible at all when building up a property portfolio. In this context, we discuss with our clients again and again whether a diversification or a focusing strategy makes sense. Our experience is that many families do better with a focusing strategy on one or a few locations and on one sector than with a multi-sector and multi-site strategy. However, the premise for this is that the locations on which one concentrates should offer long-term value stability, e.g. through sufficient population growth and attractive micro and macro locations. Similar to the structure of a securities portfolio with individual securities, each individual direct investment raises the question of the risk and return impact on the overall portfolio. According to modern portfolio theory, diversification can reduce the so-called unsystematic risk, whereby the market risk (systematic risk) is given and cannot be eliminated by diversification. The asset class of real estate is characterised by the above-mentioned characteristics and is therefore characterised by a higher, unsystematic risk. Fisher/Lorie have shown for equity portfolios that a reduction of unsystematic risk, measured as the annualised standard deviation of the portfolio, of approximately 95% can be achieved with just 20 individual stocks. By contrast, building a well-diversified real estate portfolio on the basis of direct investments requires a significantly higher number of individual securities. The development of a directly held real estate portfolio is associated with a direct real estate management task. This can be provided from the personnel resources of the foundation administration itself by setting up its own administrative apparatus or purchased externally. The development of a directly held and managed real estate portfolio is always associated with effort and corresponding costs. It has been shown that direct investment in individual properties is often less suitable for most private investors and foundations, both in terms of diversification and cost/benefit aspects. In this respect, I am happy to quote the US real estate economist Anthony Sanders: “Holding a poorly diversified real estate portfolio is more costly than holding a poorly diversified stock and/or bond portfolio”. To avoid cluster risks and to achieve efficient risk reduction, an alternative investment path is the indirect investment path via involvement in alternative real estate investment funds. Indirect real estate investments can be used to achieve efficiency benefits through economies of scale and better capital allocation due to information and specialization advantages. This has been observed among private and institutional investors and it can be observed that fund solutions have also regained in popularity and trust after the comprehensive new regulation. It can be observed, for example, that funds regulated by the KAGB and also Luxembourg fund solutions, such as the new RAIF (Reserved Alternative Investment Fund), are being well received in order to better diversify property assets.

Hill: How do you proceed when selecting investment funds?

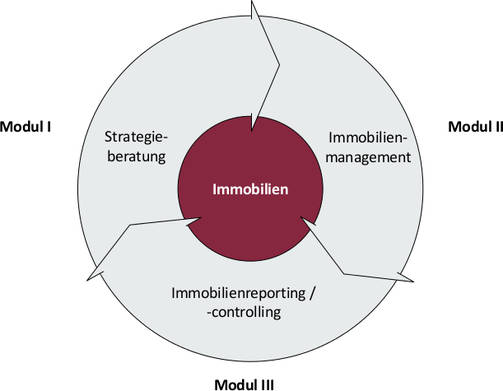

Pitschke: We also use our modular approach to fund selection. Module I involves the definition of a dedicated strategy for the real estate asset class within the framework of the overall asset allocation with further definition of the desired geographical and sectoral allocation (strategy definition). In Module II, the survey and analysis of the population of all open-ended real estate AIFs eligible for the defined investment strategy takes place. We evaluate all quantitative and qualitative information provided by the fund companies via a scoring system and subsequent fund subscription (selection process and implementation phase). In the module, we create an ongoing investment reporting system and record the fund data in a structured manner with ongoing calculation of returns.

Hill: Club deals and co-investments and mezzanine loans – is this an area where your company is active for clients?

Pitschke: Frankly, no! Not because we do not want to advise here, but because this segment has been overregulated in recent years. We are a consulting firm and not an investor ourselves. We are subject to the legal requirements of the Securities Trading Act (WpHG). Shares or participations under company law qualify as financial instruments according to WpHG. Most of our clients classify as so-called private clients according to WpHG. This group of clients, which is classified by the legislator in this way, enjoys a significantly higher level of protection than the so-called professional investors, which leads to considerable liability risks in investment advice, which requires considerable auditing and due diligence. This applies in particular to financial instruments in the form of closed investments. Many law firms today specialise in advising clients in the event of failure to sue for the reversal of their commitment. The regulatory asymmetry between the income opportunities in investment advice under MIFID II and the liability risks that are assumed is simply too great. The regulation has led to a situation in which there is less advice for investors throughout the industry with regard to financial instruments, i.e. indirect investments and in particular with regard to closed investments.

Hill: How do you currently view the venture capital and private equity sector?

Pitschke: The venture capital sector is highly interesting, but also highly speculative. Therefore, we do not go into investment consulting here, but rather we recommend to our clients network partners who have been carefully examined by us and offer very interesting investment opportunities.

Hill: How important is the current discussion about sustainability, ESG and SRI for your clients?

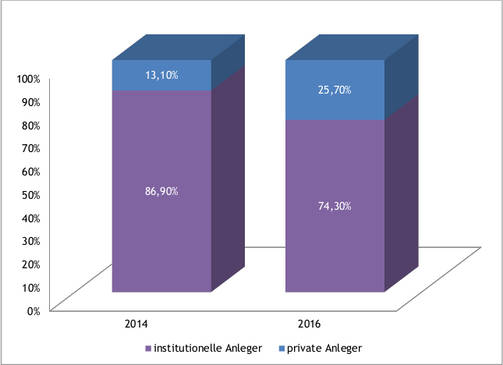

Pitschke: In the investment allocation of wealthy families, as with other investor groups, the focus is on capital preservation and yield generation. In addition to these fundamental investment motives, however, private investors are increasingly seeking to achieve a social and ethical impact from their investments. The importance of so-called sustainable investments has continued to grow across the board. In this context, we note that in the segment of sustainable investments, the proportion of private investors has increased significantly compared to institutional investors. According to a study by the Global Sustainable Investment Alliance (GSIA), the share of private investors increased from 13.1% to 25.7% from 2014 to 2016.

Source: Global Sustainable Investment Alliance (GSIA) Status: December 2016

Deutsche Oppenheim works together with ISS-oekom on the subject of sustainability. The ESG criteria relate to factors in the areas of environmental impact (E), social behaviour (S) and corporate governance (G). A large number of exclusion criteria are also taken into account. As part of its integrated sustainability approach, Deutsche Oppenheim has an “ESG Impact Reporting” prepared for the sustainable investment fund “FOS Rendite und Nachhaltigkeit” (FOS Return and Sustainability), which is updated quarterly. The ESG Impact Reporting allows, for example, a very concrete and clear comparison of the share (measured in euros) of companies in the portfolio, e.g. in fossil fuels, and how this is reflected in the MSCI All Countries World or the number of signatories to the UN Global Compact (worldwide pact concluded between companies and the UN to make globalisation more social and ecological).

Hill: Are there any current topics that are of great interest to family offices at the moment?

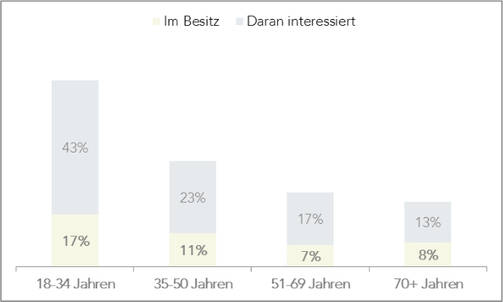

Pitschke: Yes, the topic of impact-oriented investing is playing an increasingly important role, especially in connection with the topic of sustainability. In English this impact-oriented investing is known as impact investment. This includes, for example, the reduction of poverty, food security or contributions to environmental and climate protection. Impact investors strive to achieve a certain impact as a target function and, as secondary conditions, capital preservation and a certain, but often lower than normal market interest rate. For Impact Investments, wealthy private individuals are an active but, in terms of investment volume, still a relatively small but increasingly important group of investors. Since the early days of the market, they have occasionally played a pioneering role as impact-oriented investors in Germany, as they are often able to act in a self-determined, committee-independent and flexible manner. As a rule, these are successful entrepreneurs and their families who understand the entrepreneurial approach of social entrepreneurs and can identify with it. The majority of them have been philanthropically active for a long time and often over generations. Impact investments are primarily seen as an alternative or supplement to philanthropy and donations, which makes it possible to invest capital and thereby achieve a desired positive impact. Many German Impact investors are members of a social business angel network, for example the Ashoka Support Network or investors in the Social Venture Fund. In addition, they are often actively involved as business angels in the further development of the organisations they represent. The study of US family offices on the topic of impact investing published by the US SIF Foundation impressively demonstrates the interest of younger family members in particular in investments with a certain social and ethical impact. In addition to the strong interest of young family members in Impact Investments, there is also an increased proportion of already invested individuals in this age group. At 17%, this is twice as high as in the over 51 age group.

Source: US SIF Foundation, Family Offices and Investing for Impact, 2015, p. 8.

Hill: Thank you very much for the interview.

Link to Deutsche Oppenheim: www.deutsche-oppenheim.de

Source: www.institutional-investment.de

Photo: www.pixabay.com